Last Updated December 27, 2022.

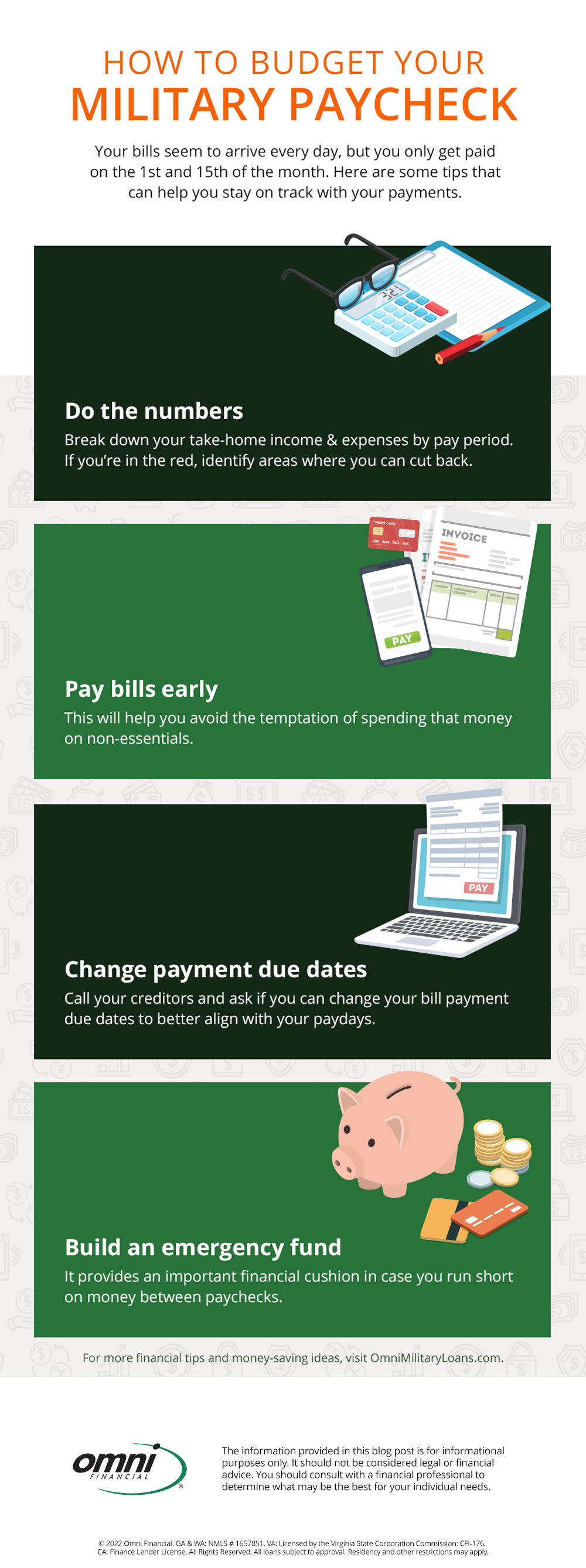

Do you run out of cash between paydays? Do you often rely on credit cards because you come up short when it is time to pay your bills? View this infographic for tips on how to get out of the paycheck-to-paycheck lifestyle.

Friendship Rewards Program

Refer a friend and get a $25 Omni Gift Card